Futures climbed 2.6 percent in New York and 2.5 percent in London. Saudi Energy Minister Khalid Al-Falih said Saturday the biggest crude exporter will “cut substantially to be below” the target agreed on last month with members of OPEC.

His comments followed a deal by 11 non-OPEC countries to join forces with the group and trim output by 558,000 barrels a day next year, the first pact between the rivals in 15 years.

U.S. oil futures have gained almost 20 percent since the Organization of Petroleum Exporting Countries agreed on Nov. 30 to cut output for the first time in eight years. Saudi Arabia, which initiated OPEC’s decision in 2014 to pump without limits, is leading efforts to regain control of the market. The OPEC and non-OPEC plan encompasses countries that produce about 60 percent of the world’s crude.

"The non-OPEC cut was expected but nobody foresaw the Saudi statement," Bob Yawger, director of the futures division at Mizuho Securities USA Inc. in New York, said by telephone. "The market’s giving bonus points because the Saudis are willing to do whatever has to be done to balance the market. We wouldn’t be up anywhere near as much on the agreement alone."

West Texas Intermediate for January delivery rose $1.33 to settle at $52.83 a barrel on the New York Mercantile Exchange. It’s the highest close since July 14, 2015. Total volume traded was about 81 percent higher than the 100-day average at 3 p.m.

Market Balance

Brent for February settlement climbed $1.36 to $55.69 a barrel on the London-based ICE Futures Europe exchange. The contract closed at the highest since July 22, 2015. The global benchmark crude ended the session at a $1.94 premium to February WTI.

"The main impact of the non-OPEC collaboration is to pull the global market into balance, if not in deficit, in the second quarter of 2017, rather than in the third quarter," said Sarah Emerson, managing director of ESAI Energy in Wakefield, Massachusetts. "On an annual average basis, this pushed the global balance into a 200,000 to 300,000 barrel-a-day deficit for the year."

Oil and gas companies advanced in the U.S. and Europe. Exxon Mobil Corp. and Chevron Corp., the biggest U.S. energy producers, climbed 1.9 percent and 0.7 percent, respectively, at 3 p.m.

“I can tell you with absolute certainty that effective Jan. 1 we’re going to cut and cut substantially, to be below the level that we have committed to on Nov. 30,” Al-Falih said Saturday in Vienna. The Saudi minister added that the country was ready to take production below 10 million barrels a day, a level it has sustained since March 2015.

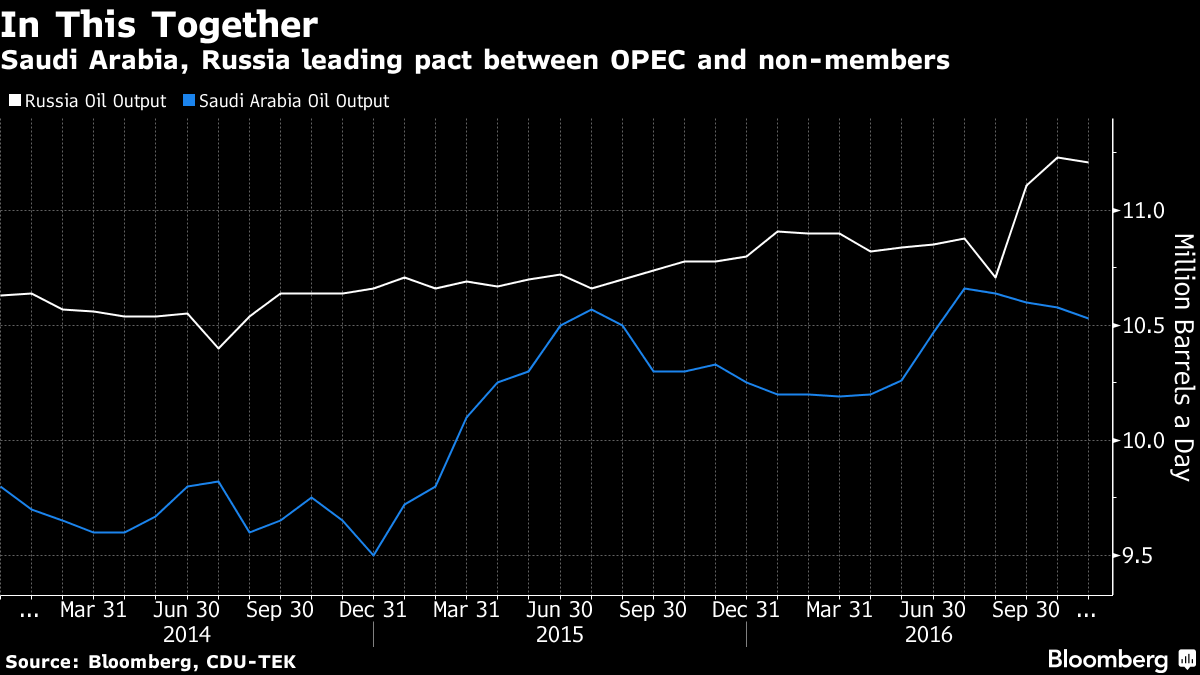

Major Players

Al-Falih and his Russian counterpart Alexander Novak also revealed Saturday that they have been working for nearly a year on the agreement, meeting multiple times in secret. OPEC two weeks ago agreed to reduce its own production by 1.2 million barrels a day, and Saudi Arabia has long insisted that any cuts by the group be accompanied by action from other suppliers.

"The Saudi statement show’s they’re really serious," Michael Lynch, president of Strategic Energy & Economic Research in Winchester, Massachusetts, said by telephone. "There’s little chance that they’ll bail if things get difficult. It’s clear they want to make this work."

Oil prices at $60 a barrel would be “ideal” for OPEC as higher levels risk sparking a recovery in competing supplies from the U.S., Nigerian Minister of State for Petroleum Emmanuel Kachikwu said in a Bloomberg Television interview.

- by Mark Shenk

No comments:

Post a Comment