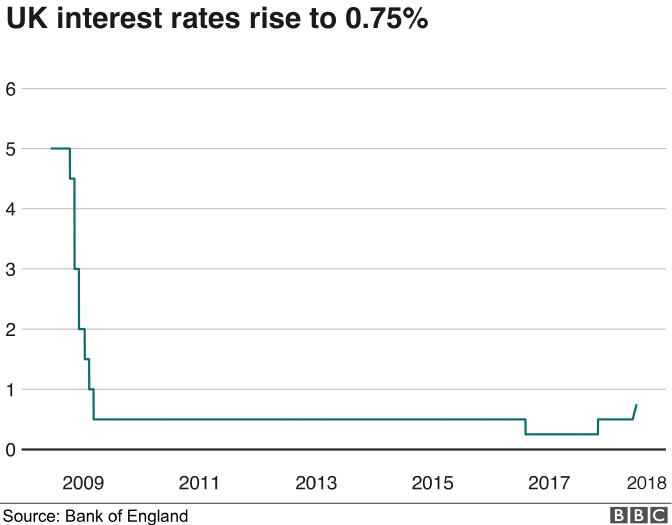

The Bank of England has raised the interest rate for only the second time in a decade.

The rate has risen by a quarter of a percentage point, from 0.5% to 0.75% - the highest level since March 2009.

The move will increase the interest costs of more than three-and-a-half million residential mortgages that have variable or tracker rates.

But it will be welcomed by savers, who will be hoping to see a rise in their interest rates over the coming months.

- What an interest rate rise means for you

- The interest rate rise is all about your wages

- Savers should not expect too much from a rate rise

- Five things we learned from the Bank of England

- Email haveyoursay@bbc.co.uk with your stories

Some business groups questioned the decision to raise the rate now ahead of the UK agreeing a Brexit deal with the European Union.

Suren Thiru, head of economics at the British Chambers of Commerce, said: "While a quarter-point rise may have a limited long-term financial impact on most businesses, it risks undermining confidence at a time of significant political and economic uncertainty."

However, the Bank of England Governor Mark Carney told the BBC that the Monetary Policy Committee (MPC) would lower the rate if the situation merited such a move.

"There are a variety of scenarios that can happen with Brexit… but in many of those scenarios interest rates should be at least at these levels and so this decision is consistent with that," he said.

"In those scenarios where the interest rate should be lower, well then the MPC which meets eight times a year would, I'm confident, take the right decision to adjust interest rates at that time."

Why are they doing this now?

The Bank's MPC had been expected to raise interest rates in May, but held fire because the economy went through a weak patch at the start of the year - partly because of the harsh weather conditions, dubbed the Beast from the East.

The Bank is now confident that the dip was temporary and that economic growth will recover from the 0.2% rate seen in the first quarter, to 0.4% in the second quarter and maintain that pace later in the year.

GETTY IMAGES

GETTY IMAGES

The Bank is sticking to previous guidance that there will be further interest rate rises, but Mr Carney said these will be "limited and gradual".

"Rates can be expected to rise gradually. Policy needs to walk, not run, to stand still," he said.

However, the Institute of Directors said the Bank had "jumped the gun" by raising the rate now.

It said: "The rise threatens to dampen consumer and business confidence at an already fragile time.

"Growth has remained subdued, and the recent partial rebound is the least that could be expected after the lack of progress in the year's first quarter."

Five interest rate facts

- More than 3.5 million residential mortgages are on a variable or tracker rate

- The average standard variable rate mortgage is 4.72%

- On a £150,000 variable mortgage, a rise to 0.75% is likely to increase the annual cost by £224

- A Bank rate rise does not guarantee the equivalent increase in interest paid to savers. Half did not move after the last rate rise

- No easy access savings account at a major High Street bank pays interest of more than 0.5%

The Bank said a pick-up in the economy is being supported by household spending, which the Bank said had been "erratic" earlier in the year.

It is also believes the recent series of store closures on the High Street does not reflect a lack of appetite for shopping.

In its Quarterly Inflation Report, the Bank said: "Although in the past year the number of retail closures have increased and retail footfall has fallen, contacts of the Bank's agents suggest that mainly reflects shifts in consumer demand to online stores and from goods to services."

Commenting on Brexit, Mr Carney said the Monetary Policy Committee "recognises that the economic outlook could be influenced significantly by the response of households, businesses and financial markets to developments related to the process of EU withdrawal".

He said: "Negotiations are now entering a critical period, with the UK and EU both seeking an agreement by the end of the year.

"Although the range of potential outcomes is wide, what matters for monetary policy is how people react to developments."

He said British households so far have been "resilient - but not indifferent - to Brexit news".

What is the outlook?

The Bank sees continuing "modest" economic growth of 1.4% this year and an increase to 1.8% next year.

The unemployment rate is expected to fall further from 4.2% and wage growth is expected to pick up.

Inflation is forecast to fall back to 2% - the Bank of England's target - by 2020.

The Bank sees some clouds on the economic horizon.

GETTY IMAGES

GETTY IMAGES

It said the outlook for the global economy was a bit gloomier, partly owing to the trade war between the US and China which has seen tariffs imposed on a range of goods.

It also highlighted a slowdown in the UK housing market this year, which has been "concentrated in London", where mortgage completions are down 12% on 2016.

But the Bank thinks that weakness might just be specific to the capital and may not say much about the prospects for the UK housing market as a whole.

What happens next?

The Bank is sticking to its guidance that interest rates will continue to head higher, but only at gradual pace and to a limited extent.

The financial markets have taken this on board and are forecasting one, and perhaps two, rises of 0.25% before 2020.

It also seems unlikely the UK will return to interest rates of 5% and above. In its inflation report ,the Bank published what it thinks is the natural interest rate for the UK economy.

It puts that at between 2% and 3%.

That relatively low rate is partly due to an ageing population.

Older people tend to save more and in the future, that will provide a greater pool of savings for lending to households and industry and help prevent the economy from overheating.

No comments:

Post a Comment