Growth was boosted by a better performance from the construction industry than previously estimated.

On an annual basis, the economy grew by 2.9% from the first quarter of 2014, up from a previous estimate of 2.4%.

The latest revision is the third estimate for the period.

For 2014 as a whole, economic growth was revised up to 3% from 2.8%.

The ONS figures showed household disposable income grew by 4.5% year-on-year, the fastest annual pace since the second quarter of 2001.

Earlier this month, the ONS said construction output in the UK was 0.2% lower in the first quarter, rather than 1.1% lower as previously estimated.

"The slight upward revision to growth in the first quarter of 2015 is down largely to the recently announced new methods to measure construction output," ONS chief economist Joe Grice said.

Quarterly growth in services output was left unrevised at 0.4%.

Howard Archer, chief UK and European economist at IHS Global Insight, forecast economic growth would accelerate in the three months to June as the uncertainty caused by the general election in May subsided.

He said he expected the economy to grow by 0.7% in the second quarter and by 2.5% over the course of the year.

The European Commission gave its blessing to Greece's imposition of capital controls on Monday, saying Athens appeared justified in temporarily breaching EU laws on free capital movement in order to protect its banks.

"As guardian of the Treaties and with a view to safeguarding the integrity of the single market, the Commission has made an immediate, preliminary assessment of the Greek measures that introduce the controls and finds them to be, prima facie, justified," Financial Services Commissioner Jonathan Hill said.

The EU executive could have raised legal objections to the measures, imposed overnight as Greece faces a default on its debt payments after talks with its creditors broke down.

However, Hill said in a statement: "In the current circumstances, the stability of the financial and banking system in Greece constitutes a matter of overriding public interest and public policy that would appear to justify the imposition of temporary restrictions on capital flows."

"Maintaining financial stability is the main and immediate challenge for the country."

Australia's treasurer Joe Hockey said the decision to join the AIIB followed extensive discussions with China

Australia has said it will join a China-led infrastructure bank as a founding member, contributing 930m Australian dollars ($718.5m; £455m) over five years.

The move will make Australia the sixth biggest shareholder of the Asian Infrastructure Investment Bank (AIIB).

More than 50 members have signed up to the lender, which is widely seen as a rival to the Western-led World Bank.

The US and Japan have refused to join, however.

Both countries have raised concerns over the bank's standards of governance, while there are concerns in the US that the AIIB could be used by China to extend its political influence.

The Beijing-based lender will help finance construction of roads, ports, railways and other infrastructure projects in Asia. The UK, France, Germany and Iran are among its members.

'Great opportunities'

Australia's decision to join "comes after extensive discussions between the government, China and other key partners around the world", said Australia's Treasurer Joe Hockey.

"The governance of the AIIB will be based on best practice, ensuring that all members will be directly involved in the direction and decision making of the bank in an open and transparent manner."

Mr Hockey said the AIIB would have paid-in capital of $20bn, "with total authorised capital of US$100bn".

The lender would provide Australia with "great opportunities to work with our neighbours and largest trading partner to drive economic growth and jobs", he added.

Legislation key to US President Barack Obama's trade agenda has been approved by the US Senate, just two weeks after it appeared to have failed.

The bill known as the Trade Promotion Authority (TPA), or more commonly "fast-track", makes it easier for presidents to negotiate trade deals.

Supporters see it as critical to the success of a 12-nation trade deal known as the Trans-Pacific Partnership (TPP).

The 60-38 vote was the product of rare Republican-White House collaboration.

The bill now awaits Mr Obama's signature.

The authority means that Congress may only vote up or down on finalised trade agreements, not amend them.

The Obama administration and many business organisations say the legislation is necessary so that trade negotiators can win lower trade barriers for US-made goods on international markets.

This fast-track bill brings the president a step closer to concluding the TPP deal with 11 other nations to remove or reduce barriers to trade and foreign investment.

How big a deal is TPP?

deal would include Japan, Malaysia, Vietnam, Singapore, Brunei, Australia, New Zealand, Canada, Mexico, Chile and Peru

have a collective population of about 800m - almost double that of the European Union's single market

the 12 nations are responsible for 40% of world trade

topics it covers include environmental protection, workers' rights, industry regulations

There are also trade talks between the US and the EU that could be expedited.

Both deals have been opposed by trade unions and many Democrats, forcing the White House to forge an alliance with congressional Republicans.

"We were really pleased to see President Obama pursue an idea we've long believed in," said Senate Majority Leader Mitch McConnell, a long-time White House foe, who once said his top priority was making Mr Obama "a one-term president".

Senate Majority Leader Mitch McConnell, a long-time political nemesis of Mr Obama, thanked the president for his efforts

Senate Finance Committee Chairman Orrin Hatch, a Republican, said the bill was "the most important bill that will pass the Senate this year".

The bills's passage - made all but inevitable after it cleared a more stringent procedural hurdle on Tuesday - incensed many Democrats.

Speaking before Wednesday's vote, Senator Sherrod Brown said the bill would lead to "corporate handouts, worker sell-outs" in the way that he said the North American Free Trade Agreement (Nafta) and other deals have done over the past two decades.

Organised labour and environmental groups have been some of the most vocal critics of the trade agreements, saying that they harm the environment and endanger US jobs.

Protests against 'fast track' have spread as far as California

However, Mr Obama and Republican leaders say that the agreements make it easier for US goods to reach global markets.

Less than two weeks ago, House Democrats and their leader, Rep Nancy Pelosi, turned against the bill in a vote that appeared to - at least temporarily - derail the president's trade agenda.

Following that, Republican leaders reworked elements of the bill and passed with large Republican and modest Democrat support.

At the central bank's policy meeting last week, it acknowledged that the exchange rate it manages is overvalued, which means it is likely to undermine economic growth, turn away tourists and hold back long-term prosperity. Yet the SNB refrained from doing anything about it, and the franc immediately appreciated even more, adding to the challenges facing the bank and Switzerland.

Because the exchange rate is a relative, not absolute, price, theSNB’s predicament is indicative of far more than domestic issues. In this particular case, the franc's strength also points to a regional misalignment that has vexed Swiss authorities for quite a while: how to retain Switzerland’s traditional standing as a safe harbor and its role as a home for foreign capital while the European Central Bank has adopted experimental monetary policies involving large-scale purchase of securities and significant expansions of its balance sheet.

The SNB cares about the exchange rate because prolonged and excessive overvaluation of the currency could lead to deindustrialization and gradually hollow out its service industry, including tourism. Small businesses suffer the most, Adding to the discomfort, .

Unlike multinational companies and many middle-sized ones, Switzerland's small businesses aren't able to relocate their production facilities abroad. And many don't rely on sufficient quantities of imported components to compensate for their currency-induced loss of competitiveness against foreign products.

Over the last few years, the SNB has tried many ways to deal with its predicament. It even took the once-unthinkable step of implementing a currency floor to ensure that the franc wouldn't strengthen beyond a certain level against the euro. Yet, what was meant as a short-term measure had to be maintained for quite a while, causing distortions elsewhere. And when the SNB felt obliged to abandon this currency arrangement last January, the decision led to unprecedented market volatility that raised doubts, at least temporarily, about the central bank’s reputation as a guardian of stability.

The SNB has also opted for negative policy interest rates -- a once- unthinkable step as well. In doing so, it has been taxing Swiss savers as it seeks to discourage inflows of foreign funds and encourage some of the nonresident capital to go elsewhere.

Last week, the central bank decided not to adopt any additional policy actions despite its exchange-rate concerns. It refrained from taking policy rates further into negative territory, concerned about the impact on the functioning of the domestic financial sector. It still has no appetite for implementing capital controls on incoming funds, a restriction that would seek to limit the inflow of foreign capital. And it doesn’t wish to impose taxes on such capital or subject it to a managed exchange rate once again.

The SNB is, in effect, trying to wait out the storm. And pending the normalization of ECB monetary policy, it hopes Switzerland will be able to cope by showing its traditional combination of resilience and agility.

Switzerland is a wealthy country and can rely on its past earnings to maintain living standards during a period of stress. It is also agile enough to partially counter the impact of exchange-rate overvaluation through a gradual internal devaluation -- that is, the acceptance by Swiss workers of lower nominal wages. And the population would accept these steps, a least for now, as part of the challenge of being a small independent and prosperous country in a tumultuous region.

The problem for Switzerland is that euro-zone monetary policy normalization is quite far away. The Greek crisis has gotten worse and is unlikely to be resolved decisively any time soon. As a result, the ECB’s next policy step is likely to involve more unconventional stimulus, which would amplify the SNB’s policy dilemma.

What the SNB (and, to a lesser extent, its Danish peer) is going through reflects a reality facing small open economies that is also a particularly consequential challenge for those in the emerging world that don't possess Switzerland’s mix of resilience and agility.

It is difficult for small open economies to come up with optimum policy responses when the big economic powers have opted to over-rely on their central banks’ use of unconventional monetary policy rather than implement comprehensive, well-balanced policy packages. With the effectiveness and credibility of international financial institutions such as the International Monetary Fund hampered by the unwillingness of big shareholders -- namely the U.S. and, to a lesser extent, Europe -- to adopt meaningful reforms, this test isn't being answered at the multinational level, either.

Visitors look at the Tokyo Stock Exchange (TSE) bourse in Tokyo June 11, 2015.

REUTERS/THOMAS PETER

Asian shares rose for a third consecutive day on Friday even as China stocks tumbled into correction territory, while the Federal Reserve's cautious stance towards lifting interest rates kept the dollar on the back foot.

Caution over Greece also tempered gains, as euro zone leaders prepared for an emergency summit on Monday to try to avert a Greek debt default.

Financial spreadbetters expected Britain's FTSE 100 .FTSE to open up 0.1 percent. Germany's DAX .GDAXI was seen up 27-38 points, or 0.2-0.3 percent, while France's CAC 40 .FCHI was seen up 2-4 points, or 0.1 percent.

A broad index of Asia-Pacific shares outside Japan .MIAPJ0000PUS gained 0.6 percent while Japan's Nikkei .N225 rose 0.9 percent from a one-month low set on Thursday.

But China shares fell heavily, tumbling more than 4 percent at one point. By midday, the key CSI300 index .CSI300 and benchmark SSEC .SSEC were down more than 9 percent for the week and over 10 percent from their early June peak.

This week's correction was triggered by regulators' fresh moves to tighten margin financing - a key engine behind the market's frenzied rally - and was worsened by a tidal wave of initial public offerings that greatly increase share supply.

"First... room for further monetary easing could be less than anticipated, and inflows of new investors could have already peaked," Bosera Asset Management Co said in a note to clients on the correction.

"Secondly, a highly-leveraged bull (market) is not sustainable," Bosera said, citing moves by the government to reduce margin loans, which the asset manager estimates have reached between 3 trillion and 4 trillion yuan.

Shares elsewhere in Asia were buoyed by views that the Federal Reserve may be more cautious about raising rates this year than earlier expected.

A moderate recovery in the U.S. economy in previous months had raised concerns the Federal Reserve would strike a hawkish stance at its meeting on Wednesday, but its cautious tone sparked a sense of relief and prompted investors to snap up risky assets.

"This removes a source of uncertainty for Asian markets in the near term and should be a positive factor going ahead, though the Greek and Chinese factors will temper any optimism," said Stephen Chiu, a strategist at Mitsubishi UFJ Financial Group in Hong Kong.

While analysts broadly concluded the Fed is on track for its first rate increase in more than a decade in September, fixed income derivatives markets such as Fed fund futures <0#FF:> expected the first hike only in December.

"The markets seem to be concluding that the Fed will raise rates only once this year, and not twice as had been priced in (before the Fed's policy meeting ended on Wednesday)," said Daisuke Uno, chief strategist at Sumitomo Mitsui Bank.

Growing expectations of a slower trajectory of U.S. interest rate increases sent the dollar swooning against a basket of currencies with the broad dollar index =USD languishing near one-month lows.

That broad undertone of caution from global investors reflected in the latest flows data. While emerging Asian bond and equity markets saw a sharp moderation in outflows from last week, overall capital flows were still in the red, according to EPFR data and ANZ strategists.

In bonds, ten-year U.S. Treasury yields US10YT=RR settled at 2.33 percent while comparable Japanese yields JP10YT=RR held at 0.44 percent.

In commodities, oil prices were a shade weaker, but plentiful output was broadly met by demand.

U.S. crude futures CLc1 edged lower to $60.41 a barrel, while Brent LCOc1 slipped 8 cents to $64.18.

Gold was sidelined at $1,199.15 an ounce XAU=.

(Additional reporting by Samuel Shen, Pete Sweeney in SHANGHAI and Hideyuki Sano in TOKYO; Editing by Kim Coghill)

New onshore wind farms will be excluded from a subsidy scheme from 1 April 2016, a year earlier than expected.

There will be a grace period for projects which already have planning permission, the Department of Energy and Climate Change said.

But it is estimated that almost 3,000 wind turbines are awaiting planning permission and this announcement could jeopardise those plans.

Energy firms had been facing an end to subsidies in 2017.

The funding for the subsidy comes from the Renewables Obligation, which is funded by levies added to household fuel bills.

After the announcement was made, Fergus Ewing, Scottish minister for business, energy and tourism and member of the Scottish parliament, said he had warned the UK government that the decision could be the subject of a judicial review.

"The decision by the UK government to end the Renewables Obligation next year is deeply regrettable and will have a disproportionate impact on Scotland, as around 70% of onshore wind projects in the UK planning system are here," he added.

'Energy mix'

The move was part of a manifesto commitment by the Conservative party ahead of the general election in May.

"We are driving forward our commitment to end new onshore wind subsidies and give local communities the final say over any new wind farms," said Energy and Climate Change Secretary Amber Rudd.

"Onshore wind is an important part of our energy mix and we now have enough subsidised projects in the pipeline to meet our renewable energy commitments," she said.

The Conservatives also say that the onshore turbines "often fail to win public support and are unable by themselves to provide the firm capacity that a stable energy system requires".

Gordon MacDougall, managing director of Renewable Energy Systems, a Sir Robert McAlpine Group company, told the BBC that "what we are seeing is political intervention".

And he criticised the intervention in what he says is the cheapest form of low-carbon energy.

The grace period could allow up to 5.2 gigawatts (GW) of wind capacity to go ahead, which could mean hundreds more wind turbines going up across the UK.

Syrians climb through a broken border fence to enter Turkey on June 14. Photographer: Bulent Kilic/AFP/Getty Images

The world hasn’t had so many refugees or internally displaced people since 1945, and numbers are expected to increase, according to an Australian research center.

About 1 percent of the global population, or about 73 million people, have been forced to leave their homes amid a spike in armed conflict over the past four years, the Institute for Economics and Peace, which compiles the Global Peace Index, said in a report published on Wednesday.

“One in every 130 people on the planet is currently a refugee or displaced and most of that comes out of conflicts in the Middle East,” institute director Steve Killelea said by phone. The numbers in Syria, where as many as 13 million of its 22 million people are displaced, are “staggering,” he said.

The number of people killed in conflict rose to 180,000 in 2014 from 49,000 in 2010; of that number, deaths from terrorism increased by 9 percent to an estimated 20,000, according to the report. The impact of this violence on the global economy, including the cost of waging war, homicides, internal security services, and violent and sexual crimes, reached $14.3 trillion in the past year, it said.

“To put into perspective, it’s 13.4 percent of global gross domestic product, equivalent to the combined economies of Brazil, Canada, France, Germany, Spain and the U.K.,” Killelea said. “It’s also more than six times the total value of Greece’s bailout and loans from the IMF, ECB and other euro zone countries combined.”

Iceland tops the index as the most peaceful country in the world, Syria as the least.

Russia has cut its main interest rate from 12.5% to 11.5% as inflation eases.

In a statement the country's central bank said it had lowered its one-week minimum auction repo rate by 1 percentage point.

Inflation eased from a high of 16.9% in March to 15.8% in May.

The bank also repeated that it was concerned about a "considerable" cooling of the economy. It said it expected gross domestic product to contract by 3.2% this year.

The Russian rouble was little changed after the rate decision as it was in line with analyst predictions.

Interest rates had hit 17% last December in an emergency move to halt a run on the rouble.

Russia's economy is being squeezed by Western sanctions over the situation in Ukraine, and a fall in global oil prices.

Photographer: Louisa Gouliamakii/AFP via Getty Images

European policy makers raised pressure on Greece to return to the negotiating table and make further concessions to unlock aid, as each side laid out its demands to rally support for its respective position.

Stocks and the euro fell on Monday as the extent of the policy divide that remains to be resolved was laid bare after weekend talks billed by European officials as a last attempt to end the standoff broke up early.

Europe needs a “strong and comprehensive agreement, and we need this very soon,” European Central Bank President Mario Draghi told lawmakers at the European Parliament in Brussels on Monday. “While all actors will now need to go the extra mile, the ball lies squarely in the camp of the Greek government to take the necessary steps.”

With signs that negotiating fatigue was stoking intransigence on all sides, some euro-area officials publicly raised the prospect of Greece’s exit from the currency region as the Greek government suggested it had reached the limits of its ability to make concessions. Finance Ministry officials from the 19-nation euro zone are due to hold a Greece call on Tuesday ahead of a meeting of ministers later this week.

“We’re reaching a potential period of turbulence if no accord is found,” French President Francois Hollande told reporters in Paris on Monday. “This is a message for Greece, because Greece mustn’t wait, it must renew talks with the institutions,” he said, referring to the International Monetary Fund, the ECB and the European Commission.

Awaiting Invitation

Greek Prime Minister Alexis Tsipras’s government said that it was awaiting an invitation from its creditors and is ready to respond anytime to continue the negotiations, according to an e-mail from the premier’s office.

The EU commission and IMF separately outlined their respective goals in the talks that broke up after just 45 minutes on Sunday. The focus now shifts to a June 18 meeting of euro-area finance ministers in Luxembourg. Officials have focused on that as a make-or-break session for Greece’s ability to avert default and stay in the currency union.

Tsipras, in a statement on Monday, portrayed Greece as the torchbearer of democracy, standing firm against creditors’ demand for pension cuts.

“One can only suspect political motives behind the fact that the institutions insist on further pension cuts, despite five years of pillaging,” Tsipras said. “We will wait patiently til the institutions adhere to realism.”

That prompted a rebuke from the European Commission.

“It is a gross misrepresentation of facts to say the institutions are calling or have called for cuts in individual pensions,” spokeswoman Annika Breidthardt told reporters in Brussels.

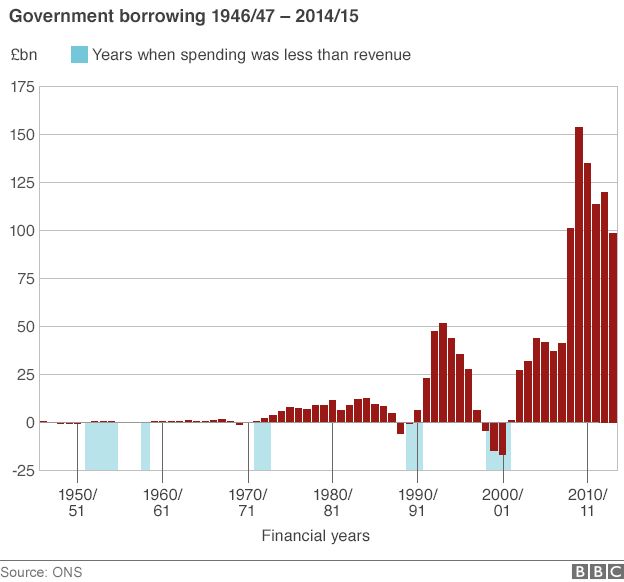

Further cuts in government spending will be needed beyond this parliament in order to bring the national debt under control, the Office for Budget Responsibility (OBR) has warned.

In its annual report, the OBR said that without further spending cuts or tax rises, the national debt would only increase.

It said a permanent £20bn cut in annual public spending will be needed by 2020.

That would help bring the national debt down to 40% of GDP by 2064, it said.

If achieved, this means it would have taken more than half a century to bring the national debt back to the same level it was before the 2008 financial crisis.

Last year, public sector net debt was £1.48tn, or 80% of economic output, compared with around £600bn, or around 42% of GDP, in 2008.

And the OBR warned that even a cut of this size, equivalent to 1.1% of GDP, would not be sufficient to keep the national debt at 40% beyond 2064.

A Treasury spokesperson responded: "Our deficit is less than half what it was, but [today's] report from the OBR clearly shows the hard work that needs to be done to fix the public finances and deliver economic security and prosperity for working people."

But the OBR cast doubt on the government's ability to maintain a surplus, forecasting the UK public sector borrowing would still be necessary by the mid 2030s as a result of the demands of an ageing population.

OBR chairman Robert Chote said the government needed to define what it meant by normal times, and that it might not be easy to calculate.

"No-one can know with confidence how much spare capacity there is in the economy or what the sustainable growth rate ... will be looking forward," he said. "Any rule needs to be defined in the knowledge that our estimates of these things may change."

The OBR said the government's triple-lock on the state pension - whereby the state pension rises by whichever is the greater of inflation, average earnings, or 2.5% - had resulted in an additional £2.9bn cost to the government, seven times higher than the £0.4bn increase originally forecast in 2010.

Earlier this week, ratings agency Moody's warned that the government will find it very difficult to achieve a budget surplus by 2018-19, and is still likely to be operating a deficit of between 1% and 2% of GDP by 2020.

Further cuts

The chancellor is due to announce spending cuts to welfare and government departments totalling £30bn over two years in his summer Budget next month.

The OBR warned if the government only made the cuts it has currently outlined, the national debt as a share of GDP would fall to 50% by the mid-2030s.

But it forecast debt to be 87% of GDP by the 2060s as a result of an ageing population, declining revenues from North Sea oil and gas, and the impact of student loans.

While admitting they were difficult to predict, the OBR forecast North Sea oil and gas revenues would fall to below 0.1% of GDP over the coming decades. It said the tax take from North Sea oil and gas had already fallen by 80% in the last three years.

That would mean a decline in revenues to £2bn in total between 2020 and 2040, down from last year's forecast of £37bn for the period.

The OBR said its latest forecast recognised the obvious collapse in oil prices in the past year but also the effect of lower production since last year.

Accumulated losses and future decommissioning costs would also impact future revenues, it said.

"Our analysis of longer-term pressures on revenue streams suggests that governments will, over time, need to find new sources of revenue to maintain the overall ratio of revenue to national income, let alone to meet the spending pressures from an ageing population," the OBR said.

People pass electronic information boards at the London Stock Exchange in the City of London October 11, 2013.

REUTERS/STEFAN WERMUTH

European shares saw fresh gains on Thursday after their best day in over a month and as bets that the United States could be edging towards its first interest rate rise kept upward pressure on global bond yields and the dollar.

At the other end of the policy spectrum, the New Zealand dollar NZD= tumbled to a five-year low after its central bank cut interest rates for the first time in four years and South Korean shares got a lift as it cut rates to new a record low.

Underlying both moves was sluggish global demand, and in particular from the region's powerhouse China.

Fixed asset investment there grew at its slowest rate in over 14 years new data showed, although industrial output and retail sales growth did show signs of steadying following a recent dive.

Europe's main bourses <0#.INDEXE> picked after a slow start with the region's benchmark FTSEurofirst 300 .FTEU3 last up 0.5 percent, as hopes returned that Greece was close to sealing a deal with its creditors. Athens' stock market surged more than 6 percent. .ATG

The euro EUR= helped too with it back down to $1.1250 as the dollar .DXY got a lift ahead of what are expected to be healthy U.S. jobless claims and retail sales data later that could nudge the Federal Reserve towards an September rate rise.

It would be its first hike in almost a decade and would finally mark a turn in the direction of the flow of easy money that has repeatedly driven world stocks and bond prices to record highs in recent years.

"The day is going to be dominated in the end by whether signs of spring in the U.S. economy have continued, will Americans come out and flash cash at last," said Kit Juckes head of global currency strategy at Societe Generale.

"And from everything overnight, its the chill from China. There could be further downside in Australia and New Zealand (currencies) and we could be talking about Asian FX weakness as a theme going forward."

KIWI CRUSH

Overnight, Tokyo's Nikkei .N225 had added 1.4 percent while Australian shares gained 1.3 percent and South Korea's Kospi advanced 0.3 percent, as they reacted to regional macro news and followed Wednesday's strong gains by Wall Street.

New Zealand's rate cut saw its dollar slide more than 2 percent on the day to a five-year low of $0.7000 NZD=D4. Most economists had not expected a cut and though traders had been saying it was going to be a close call, it got a further hit as the RBNZ said it would ease again if needed.

"The RBNZ has again proved to be more flexible than the market gives it credit for," said Michael Turner, a strategist at RBC Capital Markets.

The yen gave back some of its previous session's gains against the dollar made on comments from Bank of Japan Governor Haruhiko Kuroda who said the yen was already "very weak."

The greenback was last up 0.4 percent at 123.21 yen JPY=, but still some distance from a 13-year high of 125.86 touched Friday on robust U.S. non-farm payrolls data.

The stronger dollar meant commodities were on the back foot again with Brent oil flat at just under $66 a barrel and metals markets from industrial copper to precious gold all deep in the red.

German benchmark 10-year Bund yields DE10YT=TWEB dipped in line with the euro as has become the trend in recent months but held above the psychological 1 percent mark as higher U.S. yields US10YT=RR kept them on a tight leash.