LONDON/NEW YORK (Reuters) - After an unexpected rally that carried the dollar to 18-month peaks and saw it end 2018 as investors’ top trade, the currency faces challenges in the coming year.

They include an expensive valuation, a flagging equity boom, waning cash repatriation by U.S. companies, and the possibility that the U.S. Federal Reserve will not raise interest rates as many times as signaled.

Hence the prediction in a Reuters poll this month that the dollar will end 2019 around 5 percent below current levels..

That flies in the face of the current trend, with futures showing dollar positioning near historical highs.

Furthermore, the Bank of America Merrill Lynch’s monthly investor survey shows the greenback regaining the “most crowded trade” crown from the FAANG tech stocks group.

But the wheels have come off that investor bandwagon in recent years, as big bets have misfired on Bitcoin, tech and... the dollar, which markets had heavily bet against in late-2017.

“From a positioning perspective, the scope for the dollar to rally significantly is not there unless you see growth in the rest of the world really weakening and the United States continuing to be strong,” said Eugene Philalithis, portfolio manager at Fidelity International.

On the economic front, jobs and housing data suggest a decade-long U.S. recovery is losing traction and a flattening bond yield curve is flashing the classic recession warning.

While the Fed raised interest rates in December and signaled it would stay the course on policy tightening, money markets reckon otherwise.

Image copyrightGETTY IMAGESImage captionMr Mnuchin tweeted out details of his conversations, saying that the banks had "ample liquidity"

US Treasury Secretary Steven Mnuchin has made calls to the heads of the country's six largest banks, in an unusual move aimed at reassuring investors after big falls in US stocks.

Last week, US stocks suffered one of the worst weekly falls in a decade, as an interest rate rise and US-China trade tensions rattled markets.

Mr Mnuchin said banks confirmed they had "ample liquidity" for operations.

It also comes amid a partial government shutdown over spending plans.

"The [bank's chief executives] confirmed that they have ample liquidity available for lending to consumer, business markets, and all other market operations," the Treasury said in a statement attached to a tweet from Mr Mnuchin.

"[Mr Mnuchin] also confirmed that they have not experienced any clearance or margin issues, and that the markets continue to function properly," the Treasury's statement said.

'Strange times'

The BBC Today programme's business presenter, Dominic O'Connell, said the statement was "very odd" and could "spook markets, not reassure them".

"People are wondering whether this is really a role for the US Treasury secretary," he said.

Analysts also warned the unexpected statement could make investors nervous.

"More than anything else right now, Washington and politics are absolutely driving investor sentiment and market direction and that can turn on a dime," said Oliver Pursche, a board member at Bruderman Asset Management.

Mr Mnuchin also tried to dismiss reports that President Donald Trump had discussed the possibility of firing Federal Reserve chairman Jerome Powell, after the US central bank raised interest rates last week.

The US Treasury secretary tweeted that he had spoken to the president, who insisted he "never suggested firing" Mr Powell and did not believe he had the right to do so.

Rick Meckler, partner at Cherry Lane Investments, said the fact that Mr Mnuchin had said the White House did not have the power to remove Mr Powell, rather than saying it did not want to remove him, would be more comforting for investors.

"The administration hasn't been all that stable when it comes to changing their mind. Politically, these are very strange times," he said.

All three US indexes closed lower last week, with the technology-focused Nasdaq down 20% since its peak, placing it in so-called "bear market" territory.

US investors are worried about a range of factors including slowing economic growth at home and internationally.

In addition, a partial US government shutdown began at midnight on Friday after opposition Democrats resisted President Donald Trump's demand for $5bn (£4bn) for his Mexico border wall.

The shutdown over budget spending could continue right up to the opening of the next Congress on 3 January.

Mr Mnuchin is now set to meet with the President's Working Group on Monday, the Treasury statement said.

The group includes market regulators and Federal Reserve governors, among others. They will discuss "coordination efforts to assure normal market operations", the statement said.

Businesses that trade with the EU need to take steps now to prepare for the possibility of a no-deal Brexit, a government minister has warned.

Financial Secretary to the Treasury Mel Stride told the BBC's Today programme "there is a call to action now".

HMRC has published an update to its advice on how firms should prepare for a no-deal scenario.

However, Mr Stride called the prospect of the UK leaving the EU without a deal an "unlikely event".

Speaking to the BBC, Mr Stride said: "The time is now, there is a call to action now.

"Those who are importing or exporting into and out of the EU 27, in the unlikely event that there is a no-deal at the end of March, will need to take certain steps. They need to do that now."

Mr Stride said businesses needed to "get a customs agent on board" or "look at software they can use to make sure (of) their import and export declarations".

He added that firms should register for an Economic Operators Registration and Identification Number (EORI number) - a system of unique identification numbers used by customs authorities throughout the European Union.

Businesses should also be prepared to pay custom duties in the event of a no-deal Brexit, he warned.

The latest HMRC update marks a shift in tone, with businesses being urged to take action now.

The new version of the partnership pack also includes details about government funding for new IT systems and staff training, which is available to customs brokers, customs intermediaries and traders.

Image copyrightNIMISHA RAJAImage captionNimisha Raja, chief executive and founder of Nim's Fruit Crisps

On Wednesday, British business groups criticised politicians for focusing on infighting rather than preparing for Brexit, warning that there was not enough time to prepare for a no-deal scenario.

The groups said companies had been "watching in horror" at the continuing rows within Westminster.

Nimisha Raja, chief executive and founder of Nim's Fruit Crisps, says businesses need to be prepared for a lot more paperwork, if there is a no-deal Brexit.

Nim's Fruit Crisps sometimes has to import fruit from the EU to make its products, when fruits such as apples and pears are out of season in the UK.

"I hadn't realised quite how much we would need to do," she told the BBC.

Preparing for the changes in the import procedure was "quite an onerous task, and possibly [involving] extra cost in admin staff".

She would definitely be interested in applying for grants to ease the load.

At the moment, in order to import any item from outside the EU, importers need to locate the specific commodity code relating to each specific product.

In a no-deal scenario, this would mean British businesses would need to be able to locate commodity codes from HMRC's database, which would be time-consuming.

"Having access to funding and not having to devise it from scratch, that's brilliant. At least it would be something to start off with," said Ms Raja.

"There are possibly lots of costs involved that we haven't planned for.

"What will have a huge impact on cost will be whether you do all this yourself or whether you get an agent - but an agent will cost a lot."

South Africa’s government is facing potentially unpopular decisions needed to fix state companies that are drowning in debt, bleeding cash and fettering the economy, that may alienate voters ahead of next year’s elections. So far, it’s shied away from hard choices.

Companies such as power utility Eskom Holdings SOC Ltd., South African Airways and the South African Broadcasting Corp. are reeling after repeated management and strategy bungles and have indicated they need state aid and staff cuts to survive. While President Cyril Ramaphosa’s administration has replaced boards and top executives, it’s opposed suggestions of mass firings across the board or privatization and more bailouts at the power utility.

“There are probably going to be no major decisions and certainly no new strategies developed or started until after the election,” said Ian Cruickshanks, chief economist at the Johannesburg-based South African Institute of Race Relations. “The cost of production in all of the state-owned enterprises is going to continue escalating, the revenue will continue diminishing and if you look at what government is doing about it, the long silence means nothing.”

Electrical power lines hang from a transmission pylon in Pretoria, South Africa.

Photographer: Waldo Swiegers/Bloomberg

The May election will be the first since the ruling African National Congress forced Jacob Zuma to quit after a scandal-marred tenure that spanned almost nine years and saw its support decline. While opinion polls suggest the party’s fortunes have turned since Ramaphosa took office in February and it will easily win the vote outright, it can ill afford to alienate labor union allies that oppose job cuts and asset sales.

Looting Spree

Taxpayers would likely frown on giving state companies more money, after probes by the nation’s anti-graft ombudsman and lawmakers showed they were systemically looted of billions of rand during Zuma’s tenure. A struggling economy has also limited room to maneuver if it’s to stick to its expenditure ceiling and budget-deficit targets.

“I think they’ve got cold feet, even beyond the elections,” Ivor Sarakinsky, a senior lecturer at Johannesburg’s Wits School of Governance, said. “When they look at the numbers and the general increase in unemployment, to contribute to that by reducing the number of people inside the state-owned enterprises will have quite significant socioeconomic impact.”

Ratings companies and the nation’s auditor-general have called the parlous finances of state entities as a key risk to the economy. While Public Enterprises Minister Pravin Gordhan, who oversees the seven biggest companies, acknowledges the situation is untenable, he’s given little indication of what’s being done about it, save to say that turnaround plans are being worked on that will seek to minimize job losses.

“We have a problem, not only in Eskom but in many entities where the cost structure of the entity doesn’t justify the current operations and revenue in those entities,” Gordhan told reporters on Dec. 6.

Biggest Headache

Eskom, which provides about 95 percent of the nation’s electricity, is by far the government’s biggest headache. It’s racked up 419 billion rand ($29.5 billion) in debt, most of it state-guaranteed, isn’t selling enough power to cover its costs and has fallen behind on plant maintenance, resulting in widespread outages.

The utility employs about 48,000 people, up from 32,600 a decade ago, and a World Bank study published in 2016 found it was potentially overstaffed by 66 percent. Eskom has said it may have to fire as many as 16,000 workers and it will finalize a new strategy next year.

Ramaphosa last week named a team to help turn Eskom around after saying a bailout would boost national indebtedness. Gordhan intervened in June when a management decision to freeze pay triggered protests.

“There are critical decisions that have to be made at Eskom and it’s urgent,” said Philippa Rodseth, executive director of the Manufacturing Circle, a Johannesburg-based industry association. “It’s certainly not something that can comfortably wait until after elections because the manufacturing sector needs reliable energy supply.”

South African Airways has lost money for the past seven years. Despite having secured 19.1 billion rand in government debt guarantees and a 5 billion rand allocation in the October mid-term budget to help it repay loans, it still faces a 3.5 billion-rand cash shortfall by the end of March. Finance Minister Tito Mboweni’s suggestion that the carrier should be shut because it isn’t viable was shot down by his cabinet colleagues.

The South African Broadcasting Corp., which lost 633 million rand in the past financial year, has said it needs to fire almost a third of its 3,376 staff and 1,200 freelancers after the Treasury declined its request for 3 billion-rand cash injection. Four members of its interim board quit after the government opposed staff cuts, citing political interference in their work.

State companies will probably have to muddle though for now, with the government allocating them some additional funds from within the existing budget rather than taking the touch decisions that will benefit the economy in the long term, according to Cruickshanks.

“They are stuck in that ‘win the elections first’ mode,” he said.

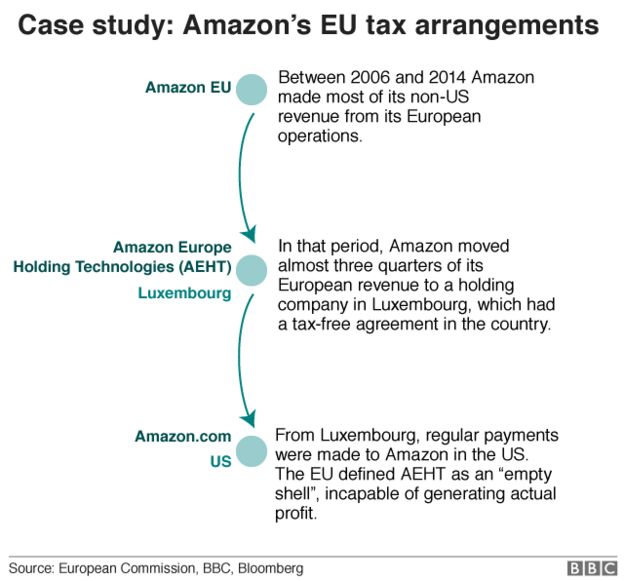

France has said it will introduce its own tax on big technology firms from 1 January after EU-wide efforts stalled.

French Finance Minister Bruno Le Maire said he expected it to bring in €500m (£450m) in 2019.

France, along with Germany, had been pushing for the European Commission to agree measures by the end of this year.

But it is opposed by countries including Ireland, the Czech Republic, Sweden and Finland.

Earlier this year, the European Commission published proposals for a 3% tax on the revenues of large internet companies with global revenues above €750m (£675m) a year and taxable EU revenue above €50m.

The move would affect companies such as Google, Apple, Facebook and Amazon.

But critics fear an EU tax could breach international rules on equal treatment for companies across the world.

EU tax reforms need the backing of all member states to become law.

Whatever the acronym, when the U.S. Federal Reserve dropped its policy rate to near zero on Dec. 16, 2008, to counter a full-scale economic crisis, it ushered in what the central bank’s chairman at the time, Ben Bernanke, called “the end of the old regime.”

A decade later, the full impact and import of that move are still not fully clear. But the Fed was never the same. The decision to move to zero ushered in wholesale changes to how the Fed works, from its building a massive balance sheet to adopting an explicit 2 percent inflation target and holding regular post-meeting press conferences.

A new body of research continues to explore the likelihood that trips to the “effective lower bound” will become common.

WHAT IS ZIRP?

It stands for “zero interest rate policy,” and became one of the most common acronyms used to describe the seven-year period when the Fed’s benchmark overnight lending rate was parked in a range of between zero and 0.25 percent. Policymakers also called it the “zero lower bound” and “effective lower bound.”

The Fed was not the first to employ such an aggressive response to an economic downturn. The Bank of Japan adopted ZIRP in the 1990s in response to a collapse in its real estate market that helped trigger a decade of economic stagnation.

WHY ADOPT ZIRP?

There was nowhere else to go. From July 2007 to the fall of 2008, the Fed had trimmed its target policy rate from 5.25 percent to 1 percent.

The economy was so weak that many models indicated the appropriate interest rate for the Fed would have been negative - in effect a tax on savings that might prompt people to spend. While theoretically possible and in fact later adopted by a few central banks elsewhere, negative interest rates would have been a political non-starter in the U.S. Congress, and difficult to sell to the public in a fast-moving crisis.

Instead, a dramatic Fed action drove the policy rate to a range of between zero and 0.25 percent. It was, in effect, a zero rate, but more importantly demonstrated the Fed's willingness to go to extremes.

DID IT WORK?

Not hardly. And Fed officials knew the developing crisis needed more than just standard interest rate policy.

“I see few advantages to gradualism,” then San Francisco Fed president Janet Yellen, the eventual chair, said according to transcripts of the December meeting. The statement announcing the cut also said the Fed “will employ all available tools to promote the resumption of sustainable economic growth.”

That flagged what was to come, including trillions of dollars in asset purchases used to shore up financial markets and maintain the low long-term interest rates that are critical to the housing market and mortgage lending. Even though the Fed could not cut its target rate any further once the "zero lower bound" had been reached, the unconventional tools used by the Fed then still shape financial markets today.

DID IT HURT?

The unemployment rate is at its lowest in nearly 50 years. Inflation is hovering around the Fed’s target. A near decade of economic growth will become the longest expansion on record next year.

What’s not to like?

It took seven years for the Fed to leave the zero lower bound, and rates are still abnormally low. By some accounts, consumers and businesses may be addicted to cheap money, and so sensitive to interest rates their willingness to buy homes or invest may fall off more quickly than in the past as rates rise.

Corporations, meanwhile, have gorged on cheap debt, possibly laying the groundwork for the next crisis.

WILL IT HAPPEN AGAIN?

Almost certainly.

The Fed has been raising interest rates now for three years, but does not expect take them much higher than 3 percent. Target policy rates of 5 percent or more were common in the past, but few at the Fed expect to return to those days.

The working assumption is that rates globally will remain lower than they were, and that policymakers will routinely reduce rates to zero in future recessions. As a consequence, they expect to keep tools like asset purchases at the ready, and are exploring other strategies, such as higher inflation targets, that could lift all rates closer to their previous levels.

The era of ZIRP, in other words, may have just begun.

Reporting by Howard Schneider; Editing by Andrea Ricci

Image copyrightAFPImage caption'Yellow vest' protests have dented the French economy

The euro has fallen against the dollar after disappointing French and German economic surveys dismayed the markets.

In France, private sector business activity contracted for the first time in two and a half years as the "gilets jaunes" protests took their toll.

In Germany, private sector activity slowed to a four-year low. The surveys pointed to weak fourth-quarter growth in the two biggest eurozone economies.

After the figures were published, the euro fell 0.6% to below the $1.13 mark.

The data came from closely-watched surveys published by research group IHS Markit, which tracks business activity across Europe in its Purchasing Managers' Index (PMI).

Any figure below 50 indicates contraction rather than expansion. The French reading confounded analysts, with the index hitting depths not seen since November 2014.

"Having held up reasonably well throughout the initial months of Q4, latest flash data pointed to an outright contraction in France's private sector for the first time in two-and-a-half years, following the protests which have swept through the country in recent weeks," said Eliot Kerr, an economist at IHS Markit.

"Momentum in the manufacturing sector's downturn gathered pace, while most notably, the service sector's resilience came to a halt, with business activity and demand dropping."

The impact of the "yellow vest" demonstrations has been keenly felt in France, where the government has been forced to bow to pressure and change its economic course.

President Emmanuel Macron has responded to the nationwide street protests by scrapping an unpopular fuel tax rise and promising an extra €100 (£90; $114) a month for minimum wage earners and tax cuts for pensioners.

However, it is far from clear that he has done enough to defuse public anger.

Bart Hordijk, market analyst at Monex Europe, said: "The sentiments among the yellow vests may have quite some support from the French public. However, businesses beg to disagree.

"If the magnitude of this drop continues in other countries and coming months, the European Central Bank's assessment that the eurozone economy 'risks moving to the downside' will quickly seem outdated, as the risks will already be there.

"The ECB president talked yesterday of 'lower growth, not of no growth'. However, a tail risk is forming that eurozone economies will slip into a recession while the ECB interest rates are still sub-zero.

"This would be a Japan-like scenario: a prospect which the euro understandably does not take well."

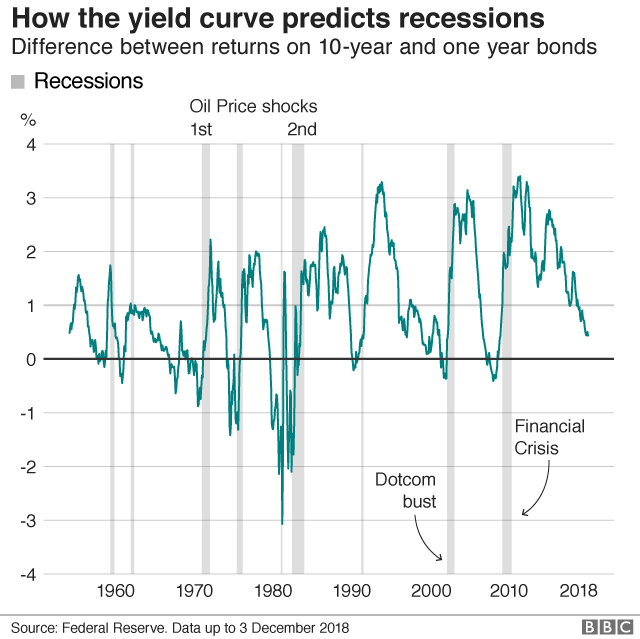

Image copyrightGETTY IMAGESImage captionInvestors increasingly fear there there could be a recession in the US

Recessions are painful. Shrinking output tends to mean huge job losses, stagnant incomes and widespread misery.

And when that recession is in the world's largest economy, it's a major headache for its trading partners, not least the UK which sells 30% of its exports to the US.

Investors are increasingly concerned there's an American recession brewing.

Of course, they, and also economists, can get it wrong. But is there a sure-fire way of predicting recessions?

Government bond markets may be one the most accurate form of financial tea leaves.

A central bank study in the US found that the bond markets had successfully foreshadowed all five US recessions since 1955.

Those bonds, known as Treasuries in the US, are issued as a form of borrowing by governments, to fund spending.

They come with different lengths of maturity - and offer investors a rate of return, paid out in regular instalments.

That rate is a fixed proportion of the ultimate value of the bond. As bonds can be freely traded, their prices change.

If demand is high, the price rises, and the bond's rate of return relative to the market price, or its yield, falls. Conversely, a lower price means a rising yield.

Healthy clip

What influences the price of bonds? Their relative attractiveness compared to other investments (if the yield is high and so price low, buyers are likely to be lured in) and also, expectations of further interest rate movements.

What does this have to do with a recession? Analysts monitor the yields of bonds across the range of maturities, right up to 30 years to plot the yield curve.

The lower the yield, the lower the expected interest rate, the worse the economy is expected to be performing.

Bonds with a longer maturity would be expected to have a higher return anyway, to compensate holders for inflation and a longer holding period.

Typically, when the outlook is for activity to expand at a healthy clip, the yield curve will slope upwards, implying interest rates on an upward trend.

But if the yield curve "inverts" - normally meaning the yield on a 10-year bond is below that of 2-year bond, it serves as an economic health warning.

But how good are these curves for predicting recessions?

Reliable indicator

The bond markets were dependable signals of all the recessions in the US since 1955.

But in the mid-1960s, the inversion of the Treasuries yield curve was followed by a slowing in activity rather than an outright contraction.

So it's not foolproof but it's probably the most reliable indicator around

What the yield curve doesn't tell us is when the US economy could go into reverse.

Over the last 60 years or so, recessions have begun from 9 to 24 months after a yield curve inverts. At present, the unemployment rate is a very modest 3.7%, while the economy continues to grow apace. But a turning point may not be far off.

What's more, predictions drawn from yield curves may be self-fulfilling.

Much as consumers react to warnings about tough times by reining in spending, banks tend to become more cautious about lending when they notice the yield curve inverting.

Less credit swilling around- in the form of mortgages, car finance, cards or corporate loans - equals less spending to fuel growth.

The warning from the bond markets should be taken seriously - and not just by those in the markets.

Capital Economics warns that there is 30% chance of the US entering recession within 18 months: just in time for the run-up to the next US presidential election.