A BNY Mellon sign is seen on their headquarters in New York's financial district, January 19, 2011.

REUTERS/BRENDAN MCDERMID

Six big U.S. banks need to raise an additional $120 billion, most likely in long-term debt, under a rule proposed on Friday by the Federal Reserve.

The requirements are aimed at ensuring that some of the biggest and most interconnected banks, which include Goldman Sachs Group Inc, (GS.N), JPMorgan Chase & Co, (JPM.N), and Wells Fargo & Co (WFC.N), can better withstand another crisis by turning some of their debt, particularly debt issued by their holding companies, into equity without disrupting markets or requiring a government bailout.

The banks are expected to meet the $120 billion shortfall by issuing debt, which is usually more cost-effective than issuing equity, according to Federal Reserve officials speaking at a background press briefing Friday. The rule proposed Friday, largely in line with banks' expectations, concerns the lenders' total loss-absorbing capacity.

It is one of a series of rules aimed at reducing risk in the banking system by determining how much debt and equity banks should use to fund themselves.

In a procedural vote, the Fed's governors approved a draft of the proposal, meaning it will be submitted for public comment.

During a public meeting with Fed officials, one staffer who worked on the rule said banks should have an easy time complying, because many requirements overlapped with existing rules. Further, the bulk of the debt requirements can be fulfilled by refinancing existing debt, the staffer said.

Some requirements must be met by Jan. 1, 2019, while more-stringent requirements must be met by Jan. 1, 2022.

The requirements are most stringent for JPMorgan, followed by Citigroup Inc. (C.N) After that come Bank of America Corp, (BAC.N) Goldman Sachs and Morgan Stanley, (MS.N) all of which have the same requirement. Wells Fargo & Co's (WFC.N) requirement is the next highest, followed by State Street Corp (STT.N) and finally Bank of New York Mellon Corp. (BK.N)

JPMorgan has more than $2 trillion in total assets, making it the largest U.S. bank by that measure.

The officials declined to say which two banks already meet the long-term debt requirements under Friday's proposal.

The rules also apply to U.S. operations of foreign globally systemically important banks, establishing roughly parallel requirements as those for U.S. banks, Fed officials said.

Also announced was a draft final rule establishing minimum margin requirements for swaps that are not cleared through an exchange. The rule is identical to one proposed by other regulators.

A Wells Fargo spokesman said in a statement the bank is reviewing the proposal and it appears to be in line with expectations. Representatives from the other banks either declined comment or were not immediately available.

US economic growth slowed sharply in the third quarter of the year.

Gross domestic product grew at an annualised pace of 1.5% between July and September, according to the Department of Commerce, down from a rate of 3.9% in the second quarter.

The slowdown was partly due to companies running down stockpiles of goods in their warehouses.

On Wednesday, the Federal Reserve kept rates unchanged and said the economy was expanding at a "moderate" pace.

Analysis: Andrew Walker, economics correspondent

Yes, it's a sharp slowdown compared with the previous three months. But the biggest reason for it was companies running down stocks - meeting demand by selling stuff they already have in the warehouse.

That is a process that has a limit. Sooner or later, they will feel they have sold enough and may want to start replenishing those stocks.

Consumer spending remained fairly robust. Yes, it too did slow, but not by all that much. It grew by 0.8% in the three-month period, or 3.2% in the annualised terms that the US official statisticians prefer.

The big question for markets is, when will the Federal Reserve raise interest rates? Will the central bank think the economy is strong enough to take it? The markets seem to think the new figures have, if anything slightly increased the chances that the Fed will move at its next policy meeting in December.

Low oil prices have hit US energy firms so far this year. But lower fuel prices have been good news for consumer spending, which accounts for more than two-thirds of US economic activity.

Consumer spending grew at 3.2% in the third quarter, down from 3.6% in the second but still a strong reading.

'Underlying strength'

Analysts said that the running down of warehouse stockpiles in the third quarter was likely to be a temporary effect and they expected growth to accelerate again in the fourth quarter.

"The headline number isn't great but this masks underlying strength," said Luke Bartholomew at Aberdeen Asset Management.

"Inventory adjustment was a drag but final domestic demand is much stronger suggesting the fundamentals of the economy remain solid."

For several months there has been intense debate about when the US central bank will raise interest rates, and now the focus is on its last meeting of the year in December.

The Fed has said in past statements that it expects to raise rates in 2015, and that labour market participation, inflation and the global economy would be the key factors in its decision.

In its latest statement on Wednesday, the Fed said: "In determining whether it will be appropriate to raise the target range at its next meeting, the committee will assess progress - both realized and expected - toward its objectives of maximum employment and 2% inflation."

However, the Fed dropped comments, which had been used in the previous month's statement, that weaknesses in the global economy could affect the US. Financial markets interpreted this as a sign that the Fed might be more likely to raise rates in December.

The Federal Reserve has decided to keep US interest rates unchanged after its latest meeting.

Federal Reserve chairwoman Janet Yellen and eight colleagues voted to keep rates where they are

The decision leaves short-term interest rates at record lows of 0% to 0.25%, the same level they have been at since December 2008.

The decision came as little surprise to the markets, although the Fed has previously signalled that rates are likely to rise within months.

The Fed said the US economy was still expanding at a moderate pace.

Share of gold mining firms were up earlier in the day on the expectation that the central bank would hold off on a rate rise this time.

In a statement, the Fed said it was continuing to watch the global economy and domestic labour market for signs of strength.

"The Committee continues to see the risks to the outlook for economic activity and the labour market as nearly balanced, but is monitoring global economic and financial developments," the statement added.

In a repeat of September's vote, nine members of the board - including chairwoman Janet Yellen - voted to keep rates the same. One, Jeffrey Lacker from the Federal Reserve Bank at Richmond, voted for an increase.

The Fed gave few hints about when it will raise rates, but if it sticks to previous expectations that a rate increase will happen this year, it has only one more chance to do so, at its next meeting in December.

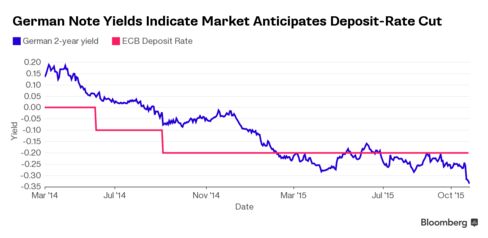

Euro-area government debt totaling $345 billion that yields less than minus 0.3 percent shows investors are looking to the European Central Bank to cut its deposit rate by a further 0.1 percentage point.

As bonds advanced across the euro zone on Tuesday, the yields that investors accepted for these very securities support the view of lenders including Deutsche Bank AG and BNP Paribas SA. The banks forecast the deposit-rate cut after ECB President Mario Draghi last week said central-bank policy makers discussed a reduction to the current rate of minus 0.2 percent, and that the officials would reexamine the scope of their quantitative-easing plan in December.

Source: Bloomberg

The ECB has ruled out buying bonds with yields below its deposit rate, which officials cut to its current level September 2014. Yet the prospect of a further reduction has helped push yields on short-dated debt still lower.

That’s because a lower deposit rate would increase the number of bonds available for the ECB to buy under QE, and traders seem to be jumping ahead of the central bank. Yields on German two-year notes dropped below minus 0.3 percent as Draghi spoke on Oct. 22.

“We’ve come a long way and now are priced about 50 percent or more for a 10 basis-point cut in December,” said Christoph Rieger, Commerzbank AG’s head of fixed-income strategy in Frankfurt, who says a reduction in the ECB rate for overnight cash is not his base case. “At this level, the market is holding its breath, waiting for more fundamental confirmation.”

Two-Year Yield

Germany’s two-year note yield declined one basis point, or 0.01 percentage point, to minus 0.34 percent at 3:38 p.m. London time, after touching a record low of minus 0.348 percent on Oct. 23, the day after Draghi’s comments. That compares to a five-year average of 0.268 percent. The price of the zero percent security due in September 2017 was at 100.64 percent of face value.

A negative yield means investors buying the securities now will get back less upon maturity than they paid.

There’s about $6.4 trillion of securities in the Bloomberg Eurozone Sovereign Bond Index, of which about 5 percent is yielding minus 0.3 percent or less.

The recent slide in yields is not limited to German debt, nor to short duration. Finland’s two-year note yield slipped to minus 0.319 percent on Tuesday, the lowest since 2001, when Bloomberg began recording it. Germany’s 10-year yield dropped five basis points on Tuesday to 0.45 percent, and touched 0.44 percent, the lowest level since May 5.

QE Effect

The introduction of the ECB’s QE program pushed the average euro-region bond yield to a record low of 0.4252 percent in March, before it rebounded in the following months, according to a Bank of America Merrill Lynch index.

The increased yields now present a challenge for policy makers, as they risk pushing the euro higher, which may threaten their efforts to revive inflation and economic growth in the 19-currency bloc. The index’s average yield was at 0.6434 percent on Monday.

China has cut its one-year benchmark interest rate by 0.25 percentage points to 4.35%.

European shares gained ground following the decision, particularly in the mining sector, and commodities rose.

The Chinese central bank also cut the ratio of Chinese currency that it expects its banks to hold.

China hopes that looser monetary policy, in the shape of cheaper money, will help it hit its growth target of 7% for 2015.

The changes will come into effect on Saturday.

Analysis by Andrew Walker, economics correspondent, BBC World Service

The decision from the People's Bank of China suggests a concern that the slowdown in growth might be becoming too abrupt.

Official figures published earlier this week told a different story. They suggested a very moderate weakening in the third quarter of the year. But Beijing's data are widely regarded as unreliable.

Lower interest rates tend to stimulate borrowing by consumers and businesses and so could contain the slowdown, but there is a risk the move could lead to a build up of debt - and some economists say China is in danger of having a financial crisis.

In London, shares in the benchmark FTSE 100 index rose 1.3%, led by miners Glencore and Fresnillo, which added 7% and 4% respectively. The Dax in Frankfurt rose 3.0%.

China's economy has grow at an average annual rate of 10% for the past three decades, but has been cooling in the past few years.

Last year it grew by 7.4%, which is extraordinary by Western standards, but a definite slowdown for China.

There is little doubt that its economy is slowing to a more sustainable rate of growth, with the question being whether that transition can be made smoothly.

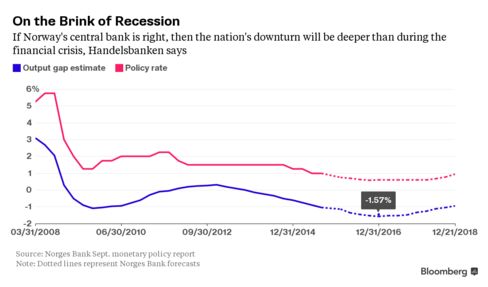

Norges Bank Governor Oeystein Olsen speaks to press after cutting rates in September.

Photographer: Krister Soerboe

With oil prices still wobbling around $50, Norway is in danger of a recession that could drive its benchmark interest rates, already at a record low, to zero.

That’s what economists at Svenska Handelsbanken AB in Oslo say as they warn that “recessionary risks are significant.” The central bank in September cut rates to 0.75 percent and signaled more than a 50 percent chance for a third reduction since the drop in oil prices accelerated, about a year ago. Handelsbanken sees three cuts next year, bringing the benchmark to zero by the end of 2016.

“The Norwegian economy will now experience a deeper downturn than during the financial crisis, with output expected to stay below its potential for longer than it did last time,” Kari Due-Andresen and Knut Anton Mork, economists at Handelsbanken, wrote in their latest report.

Besides the obvious point that Norges Bank is competing with other banks in the developed world that have cut rates to historically low levels, there are two drivers that could bring Norway’s rates even lower:

1. A krone that just can’t get weak enough.

The currency has lost 11 percent in the last year against the euro, driven down by the 43 percent drop in Brent crude to about $48 a barrel. While that has served as a “shock absorber,” buoying exporters and helping competitiveness, weak global demand means the impact of that on GDP has been modest, according to Handelsbanken.

“We can't expect non-oil sectors to meaningfully counteract the oil brake currently hitting the mainland economy,” Due-Andresen says. Further weakening of the krone is dependent on rates at zero, she says.

2. Investments dropping more than expected.

Before the big oil price drop even got started, Norway was already battling a bigger-than-expected fall in investments. Now, with Brent crude lower still, investments by oil and gas companies operating in Norway are set to suffer.

Handelsbanken even sees “new challenges” for the first phase of the nation’s Johan Sverdrup oil field. As the biggest offshore project in decades, the field is providing the nation’s oil sector a lifeline through contracts in the run-up to production, scheduled to start at the end of 2019.

Government borrowing fell in the first six months of the financial year, official figures have shown.

Public sector net borrowing excluding public sector banks was £46.3bn between April and September, down £7.5bn, or 13.9%, from a year earlier, the Office for National Statistics (ONS) reported.

In September, borrowing was £9.4bn, down £1.6bn from a year earlier.

That would be down 22.9% from the estimate of £89.2bn from 2014-15.

There was good news for the chancellor, as August's borrowing figure was revised down by £500m and July's was lowered by £2.5bn, although the figures for April and May both increased by £800m.

Analysis: Andy Verity, economics correspondent

September's public sector finances look encouraging at first sight. The government's still spending far more than its income of course. To make up the difference, it's had to borrow £46.3bn in the first six months of the financial year (April to September). But that is £7.5bn less than last year and better than most analysts expected.

This must be because of spending cuts, right?

Wrong. Spending has gone up. Departments spent 0.8% more on goods and services than last year. And spending on social benefits increased, largely because of spending on state pensions (where the triple lock promises a rise of at least 2.5% in the basic state pension).

No, it was higher tax receipts that improved the position. Income tax, national insurance and VAT receipts grew faster than the economy - by at least 4%. And, notably, corporation tax receipts rose by 7.9%.

But while there has been a cut in the amount the government has to borrow to cover its spending, it's not deep enough to hit the target. The chancellor is aiming to get borrowing down to £69.5bn for the whole year, a 23% cut. So far this year, in spite of the improved tax receipts, it's only down by 14%.

The ONS warns it is hard to use the figures for the year so far to estimate whether the government is on track to meet the OBR forecast. There are still six months of data to come, and much depends on the spike in tax receipts that is usually seen in January.

Vicky Redwood at Capital Economics said: "If the current trend continues, borrowing in 2015-16 as a whole will come in at about £78bn, much lower than 2014-15's total.

"Admittedly, this would be above the OBR's forecast... but there is still plenty of the fiscal year to go. So there's no need for the chancellor to panic yet."

However, Samuel Tombs at Pantheon Macroeconomics said: "The fiscal consolidation is still not going to plan and we think the chancellor will have to announce more austerity in time if he is to achieve his goal of a budget surplus by 2019-20."

Workers load containers onto trucks from a cargo ship at a port in Tokyo, Japan, October 20, 2015.

REUTERS/TORU HANAI

Japan's annual export growth slowed to a crawl in September as shrinking sales to China hurt the volume of shipments, raising fears that weak overseas demand may have pushed the economy into recession.

Ministry of Finance data showed exports rose just 0.6 percent in the year to September, against a 3.4 percent gain expected by economists in a Reuters poll.

That was the slowest growth since August last year, following the prior month's 3.1 percent gain. The weak yen helped increase the value of exports, but volume fell 3.9 percent, the third straight month recording an annual decline.

Wednesday's data was the first major indicator for September and is part of the calculation of third quarter gross domestic product. A third quarter contraction would put Japan into recession, following the second quarter's negative GDP result, and could force policy makers to offer further stimulus.

"Given this data, the economy probably contracted about an annualized 0.5 percent in July-September. External demand, capital spending and inventory investment were a likely drag, while consumption picked up," said Koya Miyamae, senior economist at SMBC Nikko Securities.

China's slowdown and soft domestic demand weighed on factory output and the broader economy, although the Bank of Japan saw the effects of China's slowdown as limited for now, sticking to its rosy growth outlook.

Still, weak indicators will keep the central bank under pressure to ease policy again to hit its ambitious 2 percent inflation target next year.

Some analysts expect the BOJ to move at its Oct. 30 monetary meeting, when it also issues long-term economic and price projections.

"Weak exports were within the BOJ's expectations so this data alone could not be a trigger. But there's no doubt that pressure will mount on the BOJ to act if weakness persists," said Taro Saito, senior economist at NLI Research Institute.

Separate data by the BOJ, which captures trade movements in real terms by eliminating price effects, showed real exports rose 0.2 percent in July-September while real imports grew 2.6 percent. This suggests net exports weighed on third-quarter GDP, said Yuichiro Nagai, economist at Barclays Securities Japan.

CHINA SYNDROME HITS TRADE POWERHOUSES

China's economic growth has dipped below 7 percent for the first time since the global financial crisis, despite a barrage of stimulus measures.

Flow-on effects of the slowdown are spreading though Asia, with South Korean exports tumbling while Taiwan's export orders continued to slide recently, sapping Asia’s trade powerhouses.

The MOF data showed China-bound exports fell 3.5 percent year-on-year in September, down for a second straight month on falling shipments of light oil and car parts.

Shipments to Asia - which account for about a half of Japan's overall exports - fell 0.9 percent in September, the first annual decline in seven months.

Exports to the United States, a major buyer of Japanese products, rose 10.4 percent in September, led by shipments of cars. In volume terms, however, U.S.-bound exports fell 4.7 percent.

($1 = 119.8800 yen)

(Reporting by Tetsushi Kajimoto; Editing by Eric Meijer)

Chinese investment group SinoFortone plans to invest more than £5bn in the UK.

It will invest £2bn in Orthios Eco Parks to develop waste power and food stations, initially at Holyhead and Port Talbot in Wales.

The company also said it would invest in developing an amusement park in Ebbsfleet, Kent.

The deals coincide with Chinese President Xi Jinping's visit to Britain that starts on Monday.

Development of the amusement park should begin in 2017 and should be completed by 2020, SinoFortone said.

King prawns

The two power plants in Wales will be developed over the next three years, after which the technology will be rolled out to China and developing countries.

The modular plants take waste heat from power stations that will be used to warm water for king prawn farming. The UK currently imports king prawns.

Image copyrightGetty ImagesImage captionWaste heat will be used to warm water to grow king prawns

Other types of seafood, such as Dover Sole, will follow while the process can also be used to help grow vegetables.

The system is also designed to capture carbon dioxide emissions.

The 299 megawatt Holyhead plant in Anglesey will employ at least 500 people, as will the 349 megawatt Port Talbot plant in south Wales, Orthios chief Sean McCormick told the BBC.

Thousands more people will be employed building the plants, he said.

In exchange for the investment, Orthios will source between 50% and 60% of the materials and components needed to build the plants from China.

"We have spent five years researching and developing this model and the investment from China will help us role it out across the planet," said Mr McCormick.

"China's focus on green energy and its ability to take a long-term view [was instrumental in securing the deal]."

Image copyrightSinoFortoneImage captionThe developers hope to have the new amusement park completed by 2020

SinoFortone Group is a private company that has received support from the Chinese state for this investment.

This summer it announced a £250m provisional agreement with The London Group to invest in tourist infrastructure in the UK.

"We were impressed with the Orthios professional team and how much research and development they have invested in their unique Combined Food and Power solution," said Dr Peter Zhang, SinoFortone chief executive.

"Orthios have developed a modular, efficient and scalable deliverable solution for food and power production.

"With us and the Chinese state as their backers, we are confident we can maximize efficiencies and provide a production facility to deliver this solution around the world."

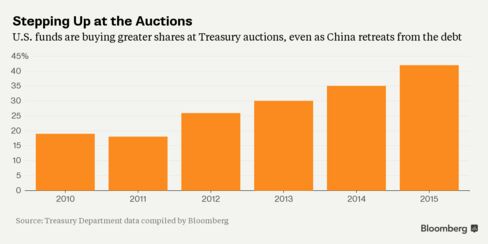

For all the dire warnings over China’s retreat from U.S. government debt, there is one simple fact that is being overlooked: American demand is as robust as ever.

Not only are domestic mutual funds buying record amounts of Treasuries at auctions this year, U.S. investors are also increasing their share of the $12.9 trillion market for the first time since 2012, data compiled by Bloomberg show.

The buying has been crucial in keeping a lid on America’s financing costs as China -- the largest foreign creditor with about $1.4 trillion of U.S. government debt -- pares its stake for the first time since at least 2001. Yields on benchmark Treasuries have surprised almost everyone by falling this year, dipping below 2 percent last week. The 10-year note yielded 2.04 percent at 12:12 p.m. in Tokyo Monday.

It’s not the scenario that doomsayers predicted would leave the U.S. vulnerable to China’s whims. But the fact that Americans are pouring into Treasuries may point to a deeper concern: the world’s largest economy, plagued by lackluster wage growth and almost no inflation, just isn’t strong enough for the Federal Reserve to raise interest rates.

“As you develop a more pessimistic view on global growth, inflation, and rates, asset managers are going to buy Treasuries in that environment,” said Brandon Swensen, the co-head of U.S. fixed-income at RBC Global Asset Management, which oversees $35 billion.

Overseas Creditors

Overseas creditors have played a key role in financing America’s debt as the nation borrowed heavily to pull the economy out of recession. Since 2008, foreigners have more than doubled their Treasury investments and now own about $6.1 trillion.

China has led the way, funneling hundreds of billions into Treasuries as the Asian nation boomed and it bought dollars to limit the gains in its currency.

Now that’s changing.

China’s economy grew 6.9 percent in the third quarter, the slowest pace since the first three months of 2009, a government report showed Monday, even as it kept Premier Li Keqiang’s target of 7 percent growth in 2015 within reach.

This year alone, China’s holdings have fallen about $200 billion as it raises money in support of its flagging economy and stock market. If the pattern holds, it would be the first time that China has pulled back from Treasuries on an annual basis. The tally includes Belgium, which analysts say is home to Chinese custodial accounts.

The People’s Bank of China directed questions on its Treasury holdings to the State Administration of Foreign Exchange, which didn’t reply to a fax seeking comment.

The Chinese pullback has led some to raise troubling questions about the U.S.’s ability to borrow and refinance its obligations at ultra-low rates year after year. It’s also reignited long-held concerns, aired over the years by both Republican and Democratic politicians, that China’s ownership of U.S. debt is a threat to America’s independence.

Homegrown Buyers

Homegrown demand for Treasuries suggests there’s no reason to panic.

American funds have purchased 42 percent of the $1.6 trillion of notes and bonds sold at auctions this year, the highest since the Treasury department began breaking out the data five years ago. As recently as 2011, they bought as little as 18 percent.

As a group, U.S. investors of all types have also stepped up their holdings of Treasuries since they fell to a low in mid-2014. In 2015, that share has climbed 2.1 percentage points to 33.1 percent of the U.S. government debt market.

That might not sound like much, but the annual increase -- which has pushed up Americans’ holdings to a record $4.3 trillion -- would be the first since 2012.

Misplaced Worries

“The worries about China selling are misplaced,” said David Ader, the head of U.S. government-bond strategy at CRT Capital Group LLC. “This was one of the great fears of the bond market, and it’s happening and we took it in stride.”

While the appetite among Americans for the haven of U.S. debt has kept the government’s financing costs low, what’s worrisome is what it suggests about the health of the economy, according to George Goncalves, the head of interest-rate strategy at Nomura Holdings Inc., one of 22 dealers that are obliged to bid at Treasury auctions.

Lower for longer?

Sure, the U.S. is creating jobs, but a raft of disappointing indicators, from retail sales to manufacturing, suggests consumers are scaling back just as overseas demand weakens.

And wages are stagnating for many Americans. Since the recession ended, average hourly earnings have increased less than in any expansion since the 1960s. Without higher wages to spur spending, inflation has remained stubbornly low.

Price Pressures

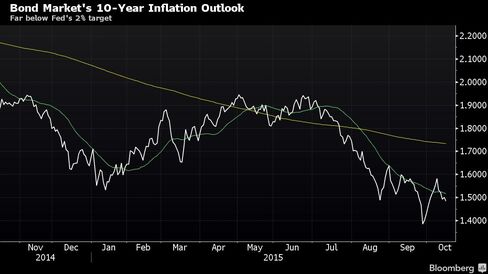

The auction data shows that U.S. funds targeted 30-year bonds -- those most vulnerable to rising growth and inflation -- the most among interest-bearing Treasuries. That comes as traders are pricing in the likelihood the inflation rate will remain below the Fed’s 2 percent goal over the coming decade.

Economists in a Bloomberg survey now see a 15 percent chance the U.S. will slide into a recession in the next 12 months, the highest estimate since 2013.

Investors in the U.S. “are making a decision based on their outlook and it’s a reflection of the economy as well as their risk aversion,” Nomura’s Goncalves said.

It also suggests the Fed policy makers may want to rethink their assumptions about the need to raise interest rates any time soon. While Fed Chair Janet Yellen has said she still sees the economy growing enough for the central bank to raise rates by year-end, traders are skeptical. They see only a 32 percent chance of a rate increase by December, while the odds of a March rise are at little more than a coin flip.

Some Fed officials are coming around to that view. Governors Lael Brainard and Daniel Tarullo both indicated this month the Fed should wait until clearer signs of inflation emerge.

“There’s no pressing reason for the Fed to hike rates and there are clear risks against a global backdrop that’s so fragile,” said Robert Tipp, the chief investment strategist at Prudential Financial’s fixed-income unit, which oversees $533 billion.