In 2007, the Icelandic economy appeared healthy. Its real Gross Domestic Product (GDP) was 35% higher than it was in 2002, unemployment was 2.3% and government debt was a modest 27% of GDP.

However, the assets of its three largest banks had grown to over nine times GDP, a size that made it impossible for the Icelandic central bank to act as an effective lender of last resort.

Thus, regardless of the quality of the banks' assets, the predictable consequence was a bank run and the subsequent collapse of the Icelandic banking system.

Following the demise of its banks, Iceland imposed capital controls to prevent massive outflows and a plunge in the value of its currency.

Intervention

Recapitalisation of its banking system and other crisis-related expenses caused government debt to rise to 95% of GDP by 2011.

However, a successful International Monetary Fund (IMF) programme cushioned the impact: real GDP fell by a less-than-expected 6.6% in 2009 and 4.1% in 2010, before returning to growth.

Icelandic authorities protected the holders of domestic deposits, who enjoyed uninterrupted access to their accounts; the UK and Dutch governments stepped in to protect deposit holders in UK and Dutch branches of Icelandic banks.

In 2013, the European Free Trade Association (Efta) court ruled that Iceland did not breach its obligations, either by treating domestic deposits differently or by not accepting legal obligation for foreign branch deposits.

Today, Iceland faces the difficult challenge of removing its capital controls in an orderly fashion but the IMF expects real GDP growth of 4.1% in 2015.

What happened in Cyprus?

In 2008, the Cypriot economy was more like that of an emerging market nation than a modern European one, but the country was enjoying an economic boom.

Cypriot real GDP had grown by 27% between 2002 and 2008. The growth, however, had been fuelled by inflows of foreign bank deposits and foreign loans to banks.

As a result, the assets of commercial banks with Cypriot parents expanded to over five times' Cypriot GDP.

Unlike the Icelandic banks, the Cypriot banks had a credible lender of last resort: their central bank was a member of the Eurosystem.

Unfortunately, they were heavily exposed to Greece.

Cypriot banks were hit hard by the restructuring of Greek sovereign debt in 2012.

Bank deposits

In March 2013, the Cypriot authorities were in a desperate situation. Either they had to make a sizable contribution to a European Stability Mechanism/IMF rescue package or the emergency loans Cypriot banks had been receiving through its central bank would be cut off.

Without the rescue package, saving the Cypriot banking system would be likely to require exiting from the euro area, adopting a new currency and recapitalising the banks by printing money.

This would cause the value of the new currency to plummet, taking with it the real value of Cypriot pensions, wages and bank accounts.

To avoid catastrophe, the Cypriot authorities looked to the one source of readily available funds: Cypriot bank deposits. Initially they planned to impose a levy on all deposits but ultimately insured depositors were spared.

To stem a run, capital controls were imposed. Banks were closed for two weeks and when they were reopened there was a limit on daily withdrawals.

Real GDP fell by 2.4% in 2012, 5.4% in 2013 and 2.3% in 2014. Unemployment rose to 16.2% in 2014 and government debt has climbed to 107% of GDP.

Currently, the outlook for Cyprus is guarded.

The country finally returned to economic growth this year and the capital controls were removed entirely in April. However, further economic reform is necessary to ensure sustainable growth.

Are there direct comparisons with Greece?

Greece currently faces a choice similar to the one faced by Cyprus in 2013.

Its banking system depends for its survival on emergency lending controlled by the ECB.

Bank runs have forced the imposition of capital controls, temporary bank closures and limits on deposit withdrawals.

The consequences of leaving the Eurosystem are likely to be as dire for Greece as they would have been for Cyprus. Reaching an accommodation with its creditors is the preferred outcome.

Real GDP has fallen by almost 30% in Greece since 2007, partly because of severe fiscal austerity.

Unemployment was 26% in 2014 and there has been an exodus of skilled labour.

As with Cyprus, and unlike with Iceland, any lasting recovery will require significant economic and fiscal reform.

Greece ranks 61st in the World Bank's Ease of Doing Business Index, edging out Russia and Cyprus (at 64) but behind Tunisia; Iceland is 12th.

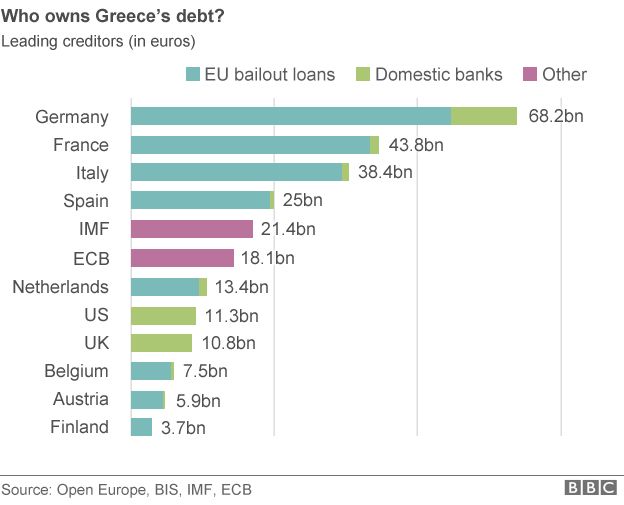

Government debt was already a massive 113% of annual GDP in 2008 and now stands at 180%.

Capital controls were necessary in Iceland and Cyprus, and in Greece today, but they come at a cost.

Many view them as an assault on civil liberties; others see them as a chance to profit.

Even in Iceland, a remote island nation, evasion and avoidance appear to have been widespread.

Some say they promote disrespect for the law and the belief that once again the wealthy, sophisticated and corrupt are benefiting at the expense of the rest of society.

Anne Sibert is a professor of Economics at Birkbeck, University of London, a fellow of the Centre for Economic Policy Research. She is a former member of the Monetary Policy Committee of the Central Bank of Iceland.

No comments:

Post a Comment